Fraud is on the rise. And if you don’t know what fraud looks like, you’re not likely to find it. While most occupational frauds are detected through tips, only 14.4% are detected by internal audit. There are more frauds uncovered by accident than by an external audit.1

Whether you’re an internal or external auditor, you realize there is little tolerance when errors and fraud go undetected, which is why many auditors are using data analysis to help identify issues within the organization’s data. The use of data analysis can help uncover fraud schemes and reduce the company’s fraud risk exposure – you just need to know where to look.

The typical organization loses 5% of its revenues to fraud each year.

– Source: Association of Certified Fraud Examiners (ACFE) 2013 Report to the Nations

Relevant information resides in financial files within the organization. The larger and more detailed the data files are, the more useful data analysis becomes. It can handle limitless amounts of data, and analysis can be performed while maintaining data integrity. Plus, most tools can track, record and provide a history of all actions performed, which is often required for court evidence.

Fraud Risk Assessment Steps

Build a profile of potential frauds to be tested

Analyze data for possible indicators of fraud

Automoate the detection process through continuous auditing/monitoring of high-risk business functions to improve controls

Investigate and drill down into emerging patterns

Expand scope and repeat as necessary

Report

So let’s start with a simple question: Why do people rob banks? Because that’s where the money is kept. The same is true for where to apply data analysis to uncover or prevent fraud. Here are some key areas where data analysis can be used to identify and get to the root cause of simple or sophisticated fraud schemes:

Payroll Fraud Schemes

While most payroll frauds are found by accident, data analysis can be used on a regular basis to analyze payments and search for outliers simply by matching payments to the payroll master file. Often fictitious or "ghost" employees are set up on a salary system to receive automatic payments.

Data to Gather:

Payroll master file with cumulative totals and static data

Monthly transactions file

Employee data including Social Security numbers, address, employee number

Data Analysis Tests to Perform:

Test for duplicate employees on the entire payroll file (appending or joining payroll files if necessary) using the employees’ SSNs as a unique employee identifier

Check for duplicate bank accounts [Note: False positives may include family accounts where more than one family member is employed by the organization]

Identify employee accounts with excessive credit memos, or large deposits

Match master information from the payroll file with the organization’s personnel file to determine whether there are "ghost" employees on the payroll

Compare the payroll file using two dates (beginning and end of the month) to determine whether new hires and terminations are represented as expected, and if any employees have received unusually large salary increases

View employee salaries by minimum and maximum by position and/or level. Also test allowances by position and level

Check for excessive overtime and allowance claims

Compare holidays/vacation and sick leave against limits by position/level

Match termination dates against the final few paychecks – look for scheme where extra checks were issued and diverted to the clerk’s account

"One of the key elements of fraud is concealment of the evidence. Our ability to aggressively and completely analyze the data we recover from suspect hard drives using IDEA has made the search for evidence much easier and more cost effective."

– Philip Levi, CFE, FCA, CPA/CFF, CA•IFA Partner, Levi & Sinclair, LLP

Purchase Frauds

Purchase frauds are prevalent, mainly because there are so many ways a potential fraudster can work the system to their advantage. Dummy invoices, reuse of valid invoices and withholding of credit notes are just a few examples of purchasing frauds. Many frauds involve the manipulation of the payments information on personal accounts within the AP system.

Examples of this include:

Creation of a fictitious supplier in the general ledger

Creation of a fictitious branch within a genuine supplier

Reactivating a dormant account

Miscellaneous accounts are particularly vulnerable, and don’t overlook frauds perpetuated on a genuine suppliers account without their knowledge. Accounts with high levels of transactions are susceptible to fraud because fictitious items can easily be buried.

Data to Gather:

Complex purchasing systems with automatic reordering capabilities are also a target. Once a supplier has been set up, or a requisition is input, payments are processed automatically. CaseWare IDEA® can be used on multiple files to test for fraud including:

Supplier master

Purchase ledger

Payments history

Purchase invoices

Supplier Master File

Using the first 5-6 characters of the name, match supplier names against a list of employee surnames from the payroll or personnel file

Test for accounts without VAT numbers or duplicate VAT numbers

Examine purchase ledger transactions for entries at or just below the management approval level – if the system finds the approving authority for a transaction, examine the value distribution for each manager

Test to see if amounts are being approved just above or below break points in authority level by a value distribution across the whole ledger

Search for split invoices to enable approvals by an individual

Extract all invoices within 90% of an approved limit and search for all invoices from that supplier. Next, sort by approving manager, department, and date to identify possible split invoices or summarize payments by invoice number to determine how many partial payments have been made for each invoice.

Test for duplicate invoices using value and supplier codes as key fields for one test, and purchase order number for another. The 2nd processing of invoices can be used to establish a value on the purchase ledger to make a fraudulent payment.

Invoices

Compare employee home addresses, SSNs, telephone numbers and bank routing/account numbers to the vendor master file

Identify invoices without a valid purchase order or from unapproved vendors

Find invoices with more than one purchase order authorization

Identify multiple invoices with the same item description

Extract vendors with duplicate invoice numbers

Find invoice payments issued on non-business days, such as weekends or holidays

Identify multiple invoices just under approval cut-off levels

Payments

Search the payments file for payees without "Inc", "LLC" and LTD" in their names to identify payments to individuals

Stratify the size of payments to extract any exceptionally high payments

If payments are made by electronic transfers, extract lists of bank codes and account numbers from both the P/L payments files and the payroll – compare to see if any accounts match

Compare voucher or invoices posted against purchase order amounts

Journals

Identify the number and value of purchase journals, particularly those transferring amounts into minor accounts

Preventing fraud and consequently minimizing financial losses, is a task that internal audit is ideally positioned to perform. IDEA can be highly effective in identifying unusual and suspect transactions within large data sets. In fact, the majority of IDEA users recover the cost of the software within the first year of use by finding duplicate payments and undetected frauds. It also saves time by automating repeatable tasks without programming.

Achieving Maximum Efficiency

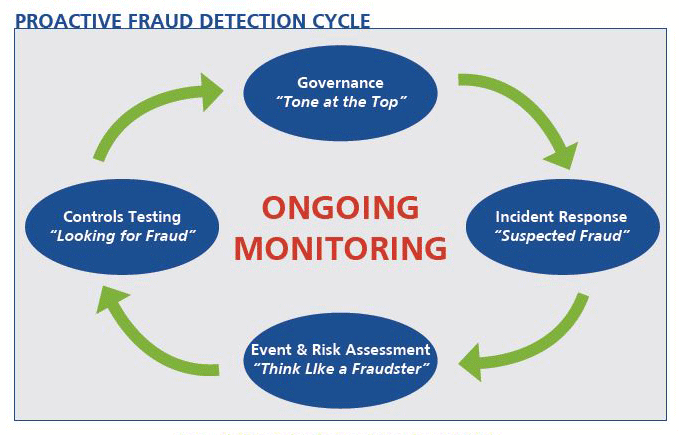

Proactive fraud detection requires moving from ad-hoc analysis towards continuous monitoring (CM). Here are some considerations for how to establish and sustain a successful CM program:

Governance: Does the culture support the CM approach? Do we have the right capabilities?

Incident Response: How will fraud be handled once it’s found?

Event & Risk Assessment: What does fraud look like within your organization?

Controls Testing: How effective are the internal controls? Are we handling ongoing changes?

By Sarah Palombo Sarah Palombo founded Avery Public Relations in 2007 and took on Audimation Services as her first client. She has more than 20 years of experience developing communications programs and creating content.

May 20 Challenges of Auditing in a Virtual World Welcome to our virtual world. These days, our company information, financial details, employee records, and client ...

Oct 27 Utilize these plugins to enhance and/or improve the automation of your workflow.

Word Find

This plugin creates a summary of all the words from...

Jan 01 A major area for government work is in auditing the various taxes collected at local and national level. Tests are often very specific to the departments concer...

BROWSER NOT SUPPORTED

This website has been designed for modern browsers. Please update. Update my browser now